Solutions / Lacima Analytics / Market Risk

Image carousel test

Model complex market behaviours simply using real-world historical patterns.

Your Historical Data Simulation (HDS) Questions

How can I model renewables, weather, or other complex variables without using complex models and calibration methods?

Can I reduce model complexity and calibration time while retaining statistical rigour and accuracy?

How can I generate realistic Monte Carlo simulations that capture historical dynamics automatically?

How can I align simulations across correlated risk factors to maintain realism across markets and instruments?

How can I better understand how historical behaviours might impact forward prices and future portfolio outcomes?

How can I handle incomplete or irregular data without losing analytical integrity?

Our Historical Data Simulation (HDS) Solution

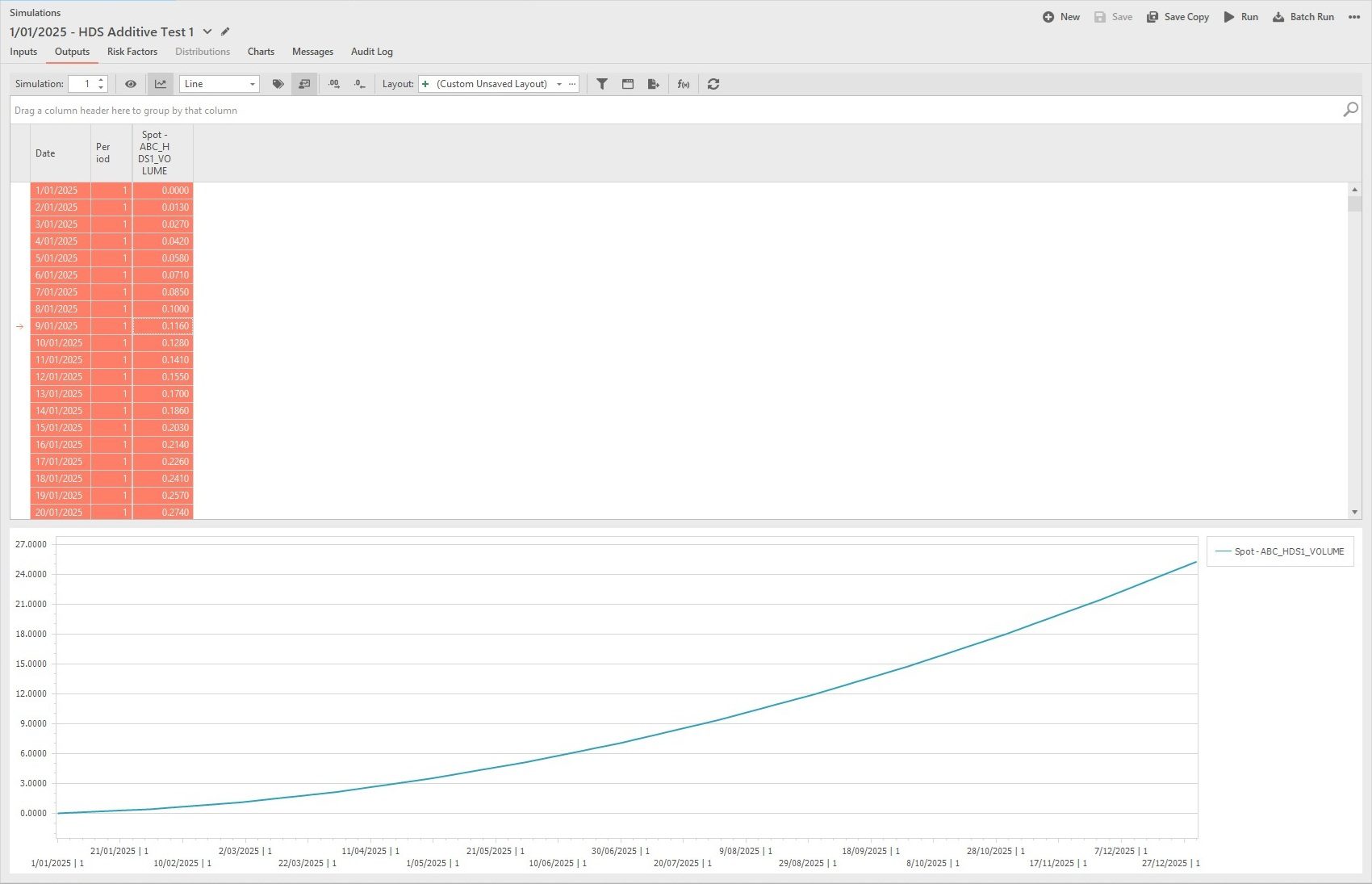

Traditionally, energy and commodity risk professionals rely on complex stochastic models that require extensive calibration, specialised parameter fitting, and repeated back-testing to ensure realism. Lacima’s Historical Data Simulation (HDS) advanced model provides a fast, simple, and intuitive alternative, allowing users to run Monte Carlo simulations directly from historical data, automatically capturing the real-world dynamics, correlations, and volatility structures embedded in past market behaviour.

This approach provides an accessible yet powerful way to model renewables, weather-driven assets, and other variables that are difficult to represent accurately through conventional calibration-based models.

Users can select historical data ranges, define block sizes, and run simulations that preserve temporal correlations and cross-factor relationships – all through a simple and easy-to-use interface.

HDS supports multiple modelling modes, Levels, Additive, and Proportional, allowing users to tailor simulations to their variable types and data structures. By combining historical realism with configurable mean adjustments and forward curve profiling, HDS delivers actionable insights into both spot and forward price behaviours under historically accurate conditions.

A streamlined user interface accelerates model setup and execution,

making advanced simulations easy and efficient to run.

The Historical Data Simulation (HDS) Features

Intuitive visual outputs bring simulated market dynamics to life,

providing actionable insight for faster, more informed decisions.

- Intuitive Historical Monte Carlo Engine

Generate simulations directly from real historical data, capturing authentic market dynamics without complex calibration. - Flexible User Interface

Configure simulation type, data periods, and block sizes for rapid model setup and testing. - Correlated Risk Factors

Simulate multiple variables together using shared historical data to preserve cross-market relationships and realism. - Robust Data Integrity and Validation

Automatically handle gaps, missing values, and inconsistencies to maintain continuity and ensure simulations are complete and accurate. - Forward Curve Integration

Link simulations with existing forward curves, supporting both automatic and relative maturities. - Mean Adjustment Controls

Align simulated outcomes with expected forward levels for improved calibration accuracy and comparability. - Comprehensive Simulation Management

Run large-scale Monte Carlo simulations efficiently within Lacima’s proven analytics framework.

Related Solutions

Lacima Analytics > EaR

Calculate and manage your cashflow-based risk metrics including Earnings-at-Risk, Gross Margin-at-Risk, Revenue-at-Risk and Profit-at-Risk.

Lacima Analytics > VaR

Easily and accurately determine Mark-to-Market value, Value-at-Risk, Greeks and position of any asset or financial contract type with a range of industry-leading valuation models.